Blue Cross Blue Shield of Illinois Enrollment Guide

How much could you save on 2022 coverage?

Compare health insurance plans in Illinois and check your subsidy savings.

Image: makam1969 / stock.adobe.com

Illinois health insurance marketplace 2022 guide

Oscar, Molina, and UnitedHealthcare enter the Illinois marketplace for 2022

- Louise Norris

- Health insurance & health reform authority

- February 25, 2022

Illinois exchange overview

Illinois uses a partnership exchange with the federal government. As of 2022, there are 11 insurers offering exchange plans in Illinois.

Frequently asked questions about Illinois's ACA marketplace

Illinois operates a partnership exchange with the federal government; the state department of insurance runs Get Covered Illinois, including a website, in-person assistance, and a help desk, and the federal government provides the IT platform – Healthcare.gov – that Illinois residents use to enroll in coverage or make changes to their plan.

Former Gov. Pat Quinn's administration announced in July 2012 that the Illinois marketplace would operate as a state-federal partnership. Quinn had hoped to leverage the partnership model as an interim step toward a state-run marketplace for the 2015 coverage year. However, a state exchange bill passed in the Senate in 2013 didn't get a vote in the House. There was some hope that exchange legislation would be considered during the fall 2014 session. However, the House did not take up the issue, and Illinois continues to have a partnership exchange (as noted above, the state's portion of the partnership was folded into the Department of Insurance in August 2015).

Rep. Robyn Gabel had hoped the issue would gain traction in 2015, given that the U.S. Supreme Court was considering whether premium subsidies could be lawfully provided in states that don't run their own health insurance exchange. By transitioning to a state-run exchange, Illinois would have secured ongoing subsidies for its residents regardless of how the Court ruled. But the Court ultimately deemed subsidies to be legal in every state, regardless of whether the federal government is running the exchange or not.

About 12% of state's population remained uninsured after the first open enrollment period. In response, officials awarded nearly $26 million to 37 organizations to target groups that were hard to reach in 2014: Latinos, African Americans, and Millennials. The efforts paid off, and Illinois' uninsured rate dropped again from 2014 to 2015.

The Trump Administration announced in mid-2017 that they would no longer fund community enrollment assistance programs in 18 cities across the country, including Chicago. The federal government also drastically reduced the advertising budget for HealthCare.gov. All of this left consumer advocates in Illinois scrambling to try to fill in the gaps and ensure that there is enough outreach and enrollment assistance available to consumers. But the Biden administration has sharply increased funding for HealthCare.gov's advertising, outreach, and enrollment assistance, and enrollment rebounded as of 2022.

As of 2022, there are 11 insurers offering exchange plans in Illinois. That includes three insurers that joined the exchange as of 2021 (Bright Health, MercyCare HMO, and SSM Health Plan/WellFirst Health) and three more that joined for 2022 (Oscar, Molina, and UnitedHealthcare).

The following insurers offer plans in the Illinois exchange for 2022, with plan availability varying from one location to another:

- Celtic Insurance Co. (Ambetter)

- Health Alliance Medical Plans, Inc. (HAMP)

- Health Care Service Corporation (HCSC, Blue Cross Blue Shield of Illinois)

- Cigna

- Quartz

- Bright Health

- MercyCare HMO

- SSM Health Plan (WellFirst Health)

- Oscar (new for 2022 in Cook, DuPage, and Lake counties)

- Molina (new for 2022)

- UnitedHealthcare (new for 2022; UHC previously participated in the Illinois marketplace, but left at the end of 2016)

The 11 insurers are offering a total of 275 plans for 2022.

Numerous states gained new marketplace insurers for 2022. But among the 33 states that use HealthCare.gov, only four states gained more than three insurers. And the Illinois marketplace also gained three new insurers as of 2021.

2014: Five insurers offered individual market plans in the Illinois exchange in 2014: Aetna, Health Care Service Corporation (Blue Cross Blue Shield of Illinois), Health Alliance, Humana, and Land of Lincoln (an ACA-created CO-OP).

2015: Time and IlliniCare joined the exchange for 2015, bringing the number of participating insurers to eight, but both insurers only offered plans for one year, exiting the exchange at the end of 2015.

2016: Time/Assurant announced in mid-2015 that they would exit the health insurance market nationwide at the end of the year, so their plans were not available for 2016.

But Aetna, Celtic, and Harken joined the market in 2016. Celtic is the sister company of IlliniCare. Aetna offered plans in the exchange in 2014 under the name Aetna Life Insurance Company, but exited for 2015. They returned for 2016 as a separate legal entity, Aetna Health Inc.

There were nine carriers offering a total of 290 plans for individuals in the Illinois exchange in 2016 (ten if you count Coventry as two separate carriers, which the Division of Insurance does). Three carriers — HCSC, Land of Lincoln, and Coventry — offered plans state-wide.

Health Care Service Corp (Blue Cross Blue Shield of Illinois) covers about 80 percent of the state's individual market enrollees.

BCBSIL announced in September 2015 that they would not offer their broad PPO (Blue PPO) network for ACA-compliant plans in 2016.

With Celtic's entry to the market, they were offering the lowest-priced plans in some areas. This was good news in terms of added competition, but bad news for people who kept their 2015 plans and then received smaller subsidies in areas where Celtic took over the benchmark spot with a premium lower than 2015's benchmark rate. This was the case in Cook County, where Celtic's low prices (and very limited network) meant that subsidies decreased for 2016.

There were significantly fewer plans available in Cook County for 2016, but the Department of Insurance noted that this was is primarily because "IlliniCare withdrew multiple plans that offered the same medical benefit packages with the only difference in coverage being the options to have adult dental and/or adult vision. This accounts for a reduction of 44 plans."

The Department of Insurance confirmed that there are no platinum plans available in the individual market in 2016 in Illinois. There were 81 platinum plans available in 2015, up from 25 in 2014. But they had all been discontinued as of 2016. This has been a trend nationwide, as platinum plans have tended to have very low enrollment rates compared with the other metal levels.

2017: Aetna exited the Illinois exchange at the end of 2016, as was the case in 11 of the 15 states where they offered exchange plans in 2016. UnitedHealthcare also exited the exchange, and so did Harken Health, which had offered plans in the Chicago area in 2016 (Harken also left the exchange in Georgia; Illinois and Georgia were the only two states where Harken offered plans, and they had only joined the exchanges for the first time in 2016).

In 2016, there were two separate Coventry entities offering plans in the Illinois exchange:Coventry Health & Life Insurance Co. as well as Coventry Health Care of Illinois, Inc. The Illinois Department of Insurance confirmed that Coventry would not offer plans in the exchange in 2017.

So Harken, Aetna, Coventry, and UnitedHealthcare exited at the end of 2016, and Land of Lincoln Health was placed in liquidation in the fall of 2016, with coverage ending September 30, 2016 (details on the departures are below). But Cigna joined the exchange in the Chicago area for 2017. So the Illinois exchange had five carriers offering plans for 2017, down from nine in 2016.

2018: Humana, one of the five insurers that offered plans in the Illinois exchange in 2017, exited the individual health insurance market nationwide at the end of 2017. Illinois has 13 rating areas, and Humana offered coverage in 2017 in northern Illinois, in three full areas (5, 7, and 8) and in part of rating area 10.

Celtic, HAMP, HCSC (BCBSIL), and Cigna continued to offer plans in the Illinois exchange for 2018.

2019: Celtic, HAMP, HCSC (BCBSIL), and Cigna all continued to offer plans for 2019, and they were joined by newcomer Gunderson/Quartz/Unity.

2020: The same five insurers are offering coverage, although Gunderson/Quartz/Unity's plan name in 2020 is Quartz Health Benefit Plans Corporation.

2021: Bright Health, MercyCare HMO, and SSM Health Plan (WellFirst Health) all joined the exchange in Illinois. Cigna and Celtic/Ambetter both expanded their existing coverage areas.

2022: UnitedHealthcare, Oscar, and Molina joined the exchange in Illinois (UnitedHealthcare offered plans in the marketplace previously, but had exited at the end of 2016).

According to ratereview.healthcare.gov, the following average rate changes were implemented for 2022:

- Celtic Insurance Co. (Ambetter): Average rate decrease of 3.21%.

- Health Alliance Medical Plans, Inc. (HAMP): Average rate increase of 10.09%.

- Cigna: Average rate increase of 1.57%.

- Quartz: Average rate increase of 16.45%.

- Bright Health: Average rate increase of 1.77%.

- MercyCare HMO: Average rate increase of 4.18%.

- Health Care Service Corporation, (HCSC, Blue Cross Blue Shield of Illinois): 4.92% increase

- SSM Health Plan (WellFirst Health): Rate filing details unavailable (but WellFirst continues to be on-exchange for 2022)

- Oscar: New for 2022, so no applicable rate change.

- Molina: New for 2022, so no applicable rate change.

- UnitedHealthcare: New for 2022, so no applicable rate change.

The Illinois Department of Insurance noted that the average second-lowest-cost silver plan (benchmark plan, used to determine premium subsidy amounts) decreased by 3% for 2022. For the lowest-cost bronze plan and the lowest-cost silver plan, average premiums dropped by 2% for 2022. For the lowest-cost gold plan, average premiums dropped by 6% for 2022.

There are several things to keep in mind when we talk about average rate changes:

- Official average rate change only apply to full-price plans, and very few enrollees pay full price for their coverage, as most receive premium subsidies that offset a significant portion of the cost. For enrollees who receive subsidies, net annual rate changes depend on how their own plan's rates are changing, as well as how their premium subsidy amount is changing (which depends on the cost of the benchmark plan, as well as the enrollee's projected income for the coming year).

- Even weighted average rate changes (calculated based on current enrollment) can't account for the fact that people switch plans during the open enrollment period.

- Overall average rate changes also don't account for the fact that premiums increase with age. A person who has individual market coverage for several years will continue to pay more each year — just due to the fact that they're getting older — even if their health plan's overall average rate change is 0% during that time.

- A weighted average, by definition, lumps all the plans together. But different insurers offer plans in each region, and each insurer's rate change is different. So the specific rate change that applies to a given enrollee can vary quite a bit from the average.

2015: ACA-compliant plans debuted in 2014, and premiums were mostly an educated guess. The Illinois Depart of Insurance summarized 2015 premium increases by metal level, with an average increase of 11 percent for the lowest-cost bronze plan, 2.6 percent for the lowest-cost silver plan, and 3.7 percent for the lowest-cost gold plan:

2016: According to the Illinois Department of Insurance, the average rate increase for the lowest-cost Silver plan in the Illinois exchange was 5.3% for 2016, and the average increase for the lowest-cost Bronze plan was 11.3%.

Blue Cross Blue Shield of Illinois imposed an average rate increase of 17.9% for individual market plans in 2016 (ranging from a 17.5 percent decrease to an increase of more than 49 percent). The new rates applied to 329,427 enrollees (including off-exchange). 80% of Illinois exchange enrollees had BCBSIL plans.

State-wide, the average benchmark (second-lowest-cost Silver plan) premiums were 6.1% more expensive in 2016 than in 2015, which meant average subsidies were larger too. But it's noteworthy that in the Chicago area, a Kaiser Family Foundation analysis determined that the average benchmark premium was 7.9% less expensive in 2016 than it was in 2015. This appears to be due in large part to Celtic's entry to the market and their relatively low premiums.

2017: The Illinois Department of Insurance again published details showing the average approved rate increases for 2017 based on metal levels, rather than specific to each carrier. The average rate increases for the lowest-cost plans at each metal level varied from 43% to 55%.

HHS confirmed that the average second-lowest-cost benchmark plan in Illinois would increase in price by 43 percent in 2017 (before any subsidies were applied). That was nearly double the 22% average increase across all the states that use HealthCare.gov. But in terms of actual dollar amounts, the average second-lowest-cost silver plan in Illinois (for a 27-year-old enrollee, before subsidies) was $298/month in 2017 — very much on par with the $296/month average across all HealthCare.gov states.

2018: The average rate increase was about 30%. It ranged from a 17% increase for HCSC to a 43% increase for Celtic/Ambetter (Cigna and HAMP were in the middle, with average increases of 27% and 41%, respectively). A significant portion of the rate increase for 2018 was due to the fact that the Trump administration eliminated federal funding for cost-sharing reductions (CSR) in late 2017.

2019: In October 2018, the Illinois Department of Insurance published an analysis of on-exchange health plans for 2019, including a summary of how premiums would change and information on which insurers would be offering plans in each area of the state. Average rate changes across most of the state varied between a decrease of 5% and an increase of 5%. Premiums for the second-lowest-priced silver plans (used to calculate premium subsidy amounts) decreased by 3% ( CMS pegged the decrease at 2 percent in Illinois).

Illinois Department of Insurance Director Jennifer Hammer noted that the market in Illinois was stabilizing by this point, both in terms of the rate changes for 2019 and the fact that the number of insurers in the exchange was growing from four to five. But at ACA Signups, Charles Gaba estimated that average premiums in Illinois would have dropped by about 13% if the individual mandate penalty hadn't been eliminated at the end of 2018, and if the Trump administration hadn't taken action to expand access to short-term plans and association health plans (both poetntially siphon healthy people out of the ACA-compliant risk pool, leading to higher premiums for the people who remain. But Illinois enacted legislation in late 2018 that limits short-term health plans to six-month terms).

2020: Most of the Illinois exchange insurers maintained the same coverage area from 2019 to 2020. But Gunderson/Quartz offered plans in four counties (Boone, Ogle, Stephenson, Winnebago) in 2019, and Quartz expanded into three additional counties for 2020 (Jo Daviess, Carroll, and Lee). HCSC continued to be the only insurer offering plans statewide.

The Illinois exchange had five participating insurers, with mostly localized coverage areas. The overall average approved rate change for 2020 was a decrease of 0.3%. But the average benchmark premium in Illinois was 6% lower in 2020 than it was in 2019. Premium subsidy amounts are based on benchmark premiums, so when benchmark premiums decline, subsidy amounts also decrease. When average subsidies decrease by more than overall average rates, some subsidized enrollees end up paying higher after-subsidy premiums. This reduced affordability could be part of the reason enrollment in the Illinois exchange dropped significantly from 2019 to 2020.

2021: If we only consider benchmark plan premiums (ie, the cost of the second-lowest-cost silver plan in each area), the average benchmark premium dropped by 6% in Illinois for 2021. All other factors (age, location, and income) remaining unchanged, this initially resulted in smaller average premium subsidies in Illinois for 2021. But the American Rescue Plan, which was enacted in March 2021, increased the size of premium subsidies and made them more widely available.

As is the case in most states that use HealthCare.gov, enrollment in the Illinois exchange peaked in 2016 and steadily declined through 2020. But while most states saw an uptick in enrollment during the open enrollment period for 2021 coverage, enrollment dropped again in Illinois, albeit slightly, with 291,215 people enrolled in coverage for 2021. However, enrollment has rebounded significantly for 2022. By December 15, 2021, a full month before the end of open enrollment, 310,489 people had already enrolled in 2022 coverage through the Illinois exchange. That had surpassed 2020 and 2021 enrollment, and had nearly caught up with 2019 enrollment — with a month remaining for additional people to sign up for coverage.

Here's a look at how many people have enrolled (during open enrollment each year) in private individual market plans through the Illinois exchange over the years:

- 2014: 217,492 people enrolled

- 2015: 349,487 people enrolled

- 2016: 388,179 people enrolled

- 2017: 356,403 people enrolled

- 2018: 334,979 people enrolled

- 2019: 312,280 people enrolled

- 2020: 292,945 people enrolled

- 2021: 291,215 people enrolled

- 2022: 310,489 people enrolled by December 15, with a month remaining in open enrollment

Would ACA subsidies lower your health insurance premiums?

Use our 2022 subsidy calculator to see if you're eligible for ACA premium subsidies – and your potential savings if you qualify.

Obamacare subsidy calculator *

Estimated annual subsidy

Provide information above to get an estimate.

* This tool provides ACA premium subsidy estimates based on your household income. healthinsurance.org does not collect or store any personal information from individuals using our subsidy calculator.

Lawmakers consider 'easy enrollment' program during 2022 session

In 2020, Maryland rolled out an "easy enrollment" program. The idea is to use the state tax return to let uninsured residents give the state permission to share applicable tax return data with the Medicaid office (or state-run exchange if the state has one) to determine whether the person might be eligible for free or low-cost health coverage.

Several other states have since created or are considering their own easy enrollment programs, but Illinois is the first to do so without having a state-run health insurance exchange. HB5142, under consideration by Illinois lawmakers in 2022, would create an easy enrollment program, but the state would not be able to offer a special enrollment period for marketplace plans in conjunction with the easy enrollment program (because Illinois uses HealthCare.gov, the state cannot set its own special enrollment periods; it has to follow the general special enrollment period rules that apply to all states that use the federally-run enrollment platform).

If HB5142 were to be enacted, Illinois residents could indicate on their state tax return whether they'd like their information to be shared with applicable state agencies. If the person is found to be eligible for Medicaid or CHIP, the state would be able to notify them and help them enroll, since those programs have year-round enrollment. But if they're eligible for marketplace coverage, with or without a subsidy, the state would only be able to pass that information on to the tax filer, along with information about the annual enrollment period (November 1 to January 15) and general special enrollment periods.

The legislation does note that if Illinois were to ever create its own state-run exchange, the exchange would be able to offer a special enrollment period in conjunction with the easy enrollment program.

Illinois requires more robust coverage of mammograms on state-regulated plans as of 2020

Illinois enacted legislation (SB162) in 2019 to expand on the scope of mammography coverage that must be offered at no cost to residents enrolled in state-regulated plans (self-insured group plans are regulated under federal law rather than state law, so state regulations don't apply to them; most very large employers self-insure rather than purchasing commercial health insurance).

The new law took effect in January 2020. It requires health plans to go beyond the federal preventive care mandate for mammography, which only requires insurers to cover—with no cost-sharing for the patient—screening mammograms (ie, when there is no cause for concern, and the patient is simply having a routine mammogram).

Under the new law in Illinois, insurers have to continue to fully cover screening mammograms, but also have to cover breast ultrasounds and MRIs for women with dense breast tissue or women whose doctor believes the ultrasound or MRI is medically necessary. In addition, insurers will have to fully cover (with no cost-sharing) diagnostic mammograms, which are used when an abnormality is detected in the breast, either during a screening mammogram or otherwise.

The Illinois law does include an exception for plans that are HSA-qualified and would lose their HSA-qualified status if they provided pre-deductible coverage for anything beyond what the federal government considers preventive care. And as is the case with any insurance mandates, it only applies to state-regulated plans (ie, plans that aren't self-insured).

Land of Lincoln CO-OP closed in 2016

In July 2016, regulators at the Illinois Department of Insurance announced that they would be taking over Land of Lincoln Health—an ACA-created CO-OP—and establishing an orderly wind-down of the carrier's business. Land of Lincoln plans were no longer for sale in Illinois as of July, and the CO-OP was placed in liquidation on September 29, with coverage for existing members ending on September 30, 2016. The Illinois Life and Health Guaranty Association covered Land of Lincoln claims (beyond the insurer's assets), but announced in 2018 that they would no longer accept any new claims for Land of Lincoln insureds or providers.

The state worked with HHS to implement a special enrollment period for Land of Lincoln's 49,000 members so that they would be able to transition to new plans.

In Oregon and New York, when CO-OPs closed mid-year, other carriers in the state agreed to enroll the CO-OP members and credit them for the out-of-pocket costs they had incurred to that point in the year. But that did not happen in Illinois.

Blue Cross Blue Shield of Illinois — by far the largest insurer in the state's individual market — said they would not be able to credit Land of Lincoln members for out-of-pocket costs they've already incurred in 2016 if the members switched to BCBSIL starting in October. The state noted that it did not have the power to force carriers to give transitioning CO-OP members credit for their out-of-pocket costs for the first three quarters of 2016, and no other carriers said they would do so. The result was that CO-OP members who had already incurred charges in 2016 had to start over again on their out-of-pocket exposure for the year as of October 1, under the new plan they selected. And then they had to start over again just three months later, on January 1, paying towards 2017's out-of-pocket exposure.

In April 2017, Illinois regulators reached out to previous Land of Lincoln members, explaining that they could file claims against the liquidated assets of the CO-OP if they could demonstrate that they suffered a loss as a result of the mid-year shutdown. CO-OP members who had to start over with their deductibles and other out-of-pocket costs in October were the primary examples of people who could file a claim, although there was no guarantee that they would recoup the money they lost.

By the end of 2015, 12 of the original 23 CO-OPs created by the ACA had closed. And although Land of Lincoln Health was not among them, the CO-OP ceased individual and small group enrollments for 2016 mid-way through the open enrollment period, noting that they had already met their enrollment target for the year (Community Health Alliance in Tennessee did the same thing during the 2015 open enrollment period; ultimately they were one of the CO-OPs that shut down at the end of 2015).

Land of Lincoln Health lost $90.8 million in 2015, on the heels of a $17.7 million loss in 2014. And 44 percent of the CO-OP's 2015 losses occurred in the fourth quarter of the year; losses had been at $50 million as of September 2015. Their losses in 2015 were the highest of all the CO-OPs that were still operational as of the start of 2016.

In 2014, Land of Lincoln Health struggled with low enrollment, with just 3,461 members at the end of 2014 (only about 4 percent of their target). But that changed dramatically in year two. For 2015, Land of Lincoln Health lowered their premiums by 20 to 30 percent, and in most areas of the state, they offered the lowest-priced silver plans.

As a result, their membership ballooned to 50,000 people by the end of the 2015 open enrollment period. Most of them — about 80% — had individual market plans, while the rest had small group plans that averaged about 8 to 10 employees each. By the end of 2015, the CO-OP had about 20% of the exchange market in Illinois, and about 10% of the entire individual market in the state.

During the first six months of 2015, Land of Lincoln Health paid out $26 million more in claims than they collected in premiums. In October 2015, HHS announced that carriers across the country – including CO-OPs – would get only 12.6% of what they were owed under the risk corridors program. Land of Lincoln sued the federal government in June 2016 over the still-unpaid risk corridor money, but the case was thrown out by a federal judge in November 2016, after Land of Lincoln Health had already closed down.

In June 2016, the risk adjustment payment amounts for 2015 were published, and Land of Lincoln owed $31.8 million—the second-highest amount of any of the remaining CO-OPs. But the Illinois Department of Insurance acted immediately in an effort to block the CO-OP from having to make that payment to HHS. The Department of Insurance's position was that Land of Lincoln should withhold payment for the 2015 risk corridors program until they receive the $73 million they're owed for the 2014 risk corridors program.

The letter to CMS regarding blocking the CO-OP from paying the risk adjustment bill was "designed to prevent an immediate liquidation" of Land of Lincoln. Ultimately, that strategy failed, the state of Illinois had no choice but to shut down the CO-OP.

No insurers offer SHOP plans in Illinois as of 2020 (small-group plans still available from insurers and brokers)

Illinois health insurance exchange resources

Other types of health coverage in Illinois

Medicaid in Illinois

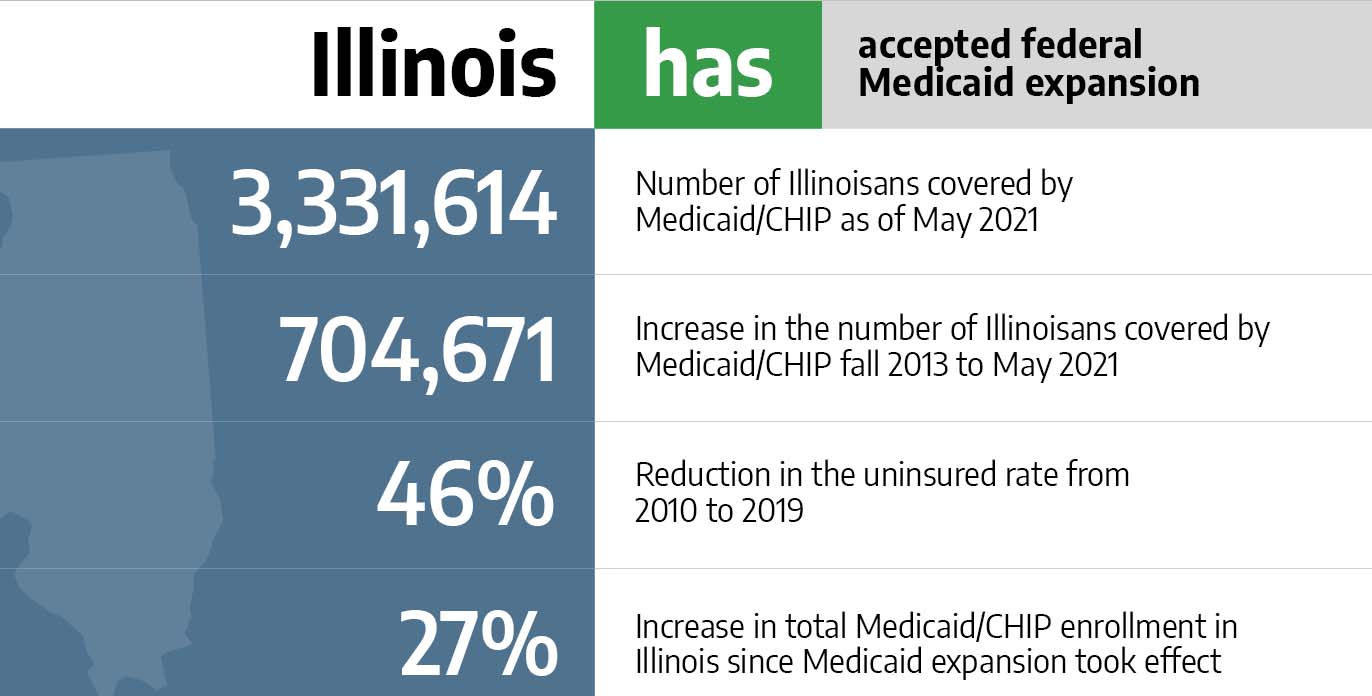

More than 780,000 people in Illinois have coverage as a result of the state's expansion of Medicaid.

Medicare in Illinois

A new "birthday rule" window provides limited plan change options for some Medigap enrollees as of 2022.

Dental Insurance in Illinois

Learn about adult and pediatric dental insurance options in Illinois, including stand-alone dental and coverage through the Illinois marketplace.

zawackislieventes.blogspot.com

Source: https://www.healthinsurance.org/health-insurance-marketplaces/illinois/

0 Response to "Blue Cross Blue Shield of Illinois Enrollment Guide"

Enregistrer un commentaire